The choice between GAAP and IFRS can significantly affect a company’s financial statements. For instance, under GAAP, the deferred charge appears as an asset, potentially inflating the company’s asset base. Conversely, IFRS’s approach results in a lower bond liability, which can affect leverage ratios and other key financial metrics. Companies operating in multiple jurisdictions must navigate these differences carefully to ensure compliance and accurate financial reporting. Software tools like QuickBooks and SAP can facilitate the amortization process by automating the calculations and ensuring compliance with accounting standards.

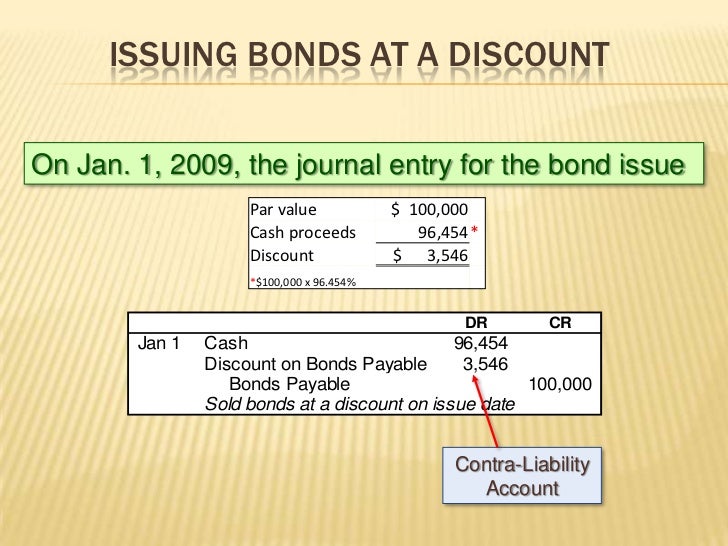

- The debt issuing cost will be recorded as the assets and amortized over the bonds life.

- We may earn a commission when you click on a link or make a purchase through the links on our site.

- Areas for further research include testing innovative interventions to improve criminal justice outcomes, such as Motivational Interviewing Case Management (MICM) and examining the community context of SLHs.

- The interest rate set on the bonds is based on the credit rating of the company and the demand from investors.

Revolver Commitment Fees are Still Treated as a Capital Asset

Voters in Le Mars on Tuesday approved a $49.97 million bond issue to build a new elementary school to replace its three aging elementary buildings. Needing 60% approval to pass, the measure bond issue costs received 61% of the vote, 4,254-2,671, to pass on its first attempt. Le Mars School District Superintendent Steve Webner is pictured in front of the district’s administration building.

Assessing the Impact of the Community Context

This includes the bond indenture, offering memorandum, and any other regulatory filings required by the Securities and Exchange Commission (SEC) or other governing bodies. Legal counsel ensures that all documentation complies with applicable laws and regulations, mitigating the risk of future legal complications. The complexity of the bond issuance, such as whether it involves multiple jurisdictions or unique financial structures, can influence the magnitude of these fees. Accurate accounting for legal fees is essential for maintaining transparency and regulatory compliance.

Debt Issuance Cost Example

The company will require to capitalize the debit issuing cost as the assets on the balance sheet when the company issue debt and paid for the fees. While debt issuance costs may seem like a minor expense, they can add up quickly, especially for large companies. As a result, it is important for companies to carefully consider all of their options before issuing new debt. One way to minimize debt issuance costs is to work with a reputable and experienced financial advisor. Using straight-line amortization, each month the corporation will debit Interest Expense for $200 ($24,000 divided by 120 months) and credit Bond Issue Costs for $200.

Impact of Issuing Bonds on the Issuer

The company spends an issuance cost $ 600,000 ( $250,000 + $ 250,000 + $ 100,000) to issue the bonds to the capital market. However, it is not allowed to amortize the debt issuance cost over the bond’s lifetime over the straight-line method. When a company takes out a loan, they agree to repay the amount borrowed, plus interest, over a period of time. Debt financing can be a good option for companies because it allows them to access the funds they need without giving up equity in the company. However, it is important to remember that debt must be repaid regardless of whether or not a company is successful. This means that companies need to carefully consider whether or not they will be able to make the required payments before taking out a loan or debt.

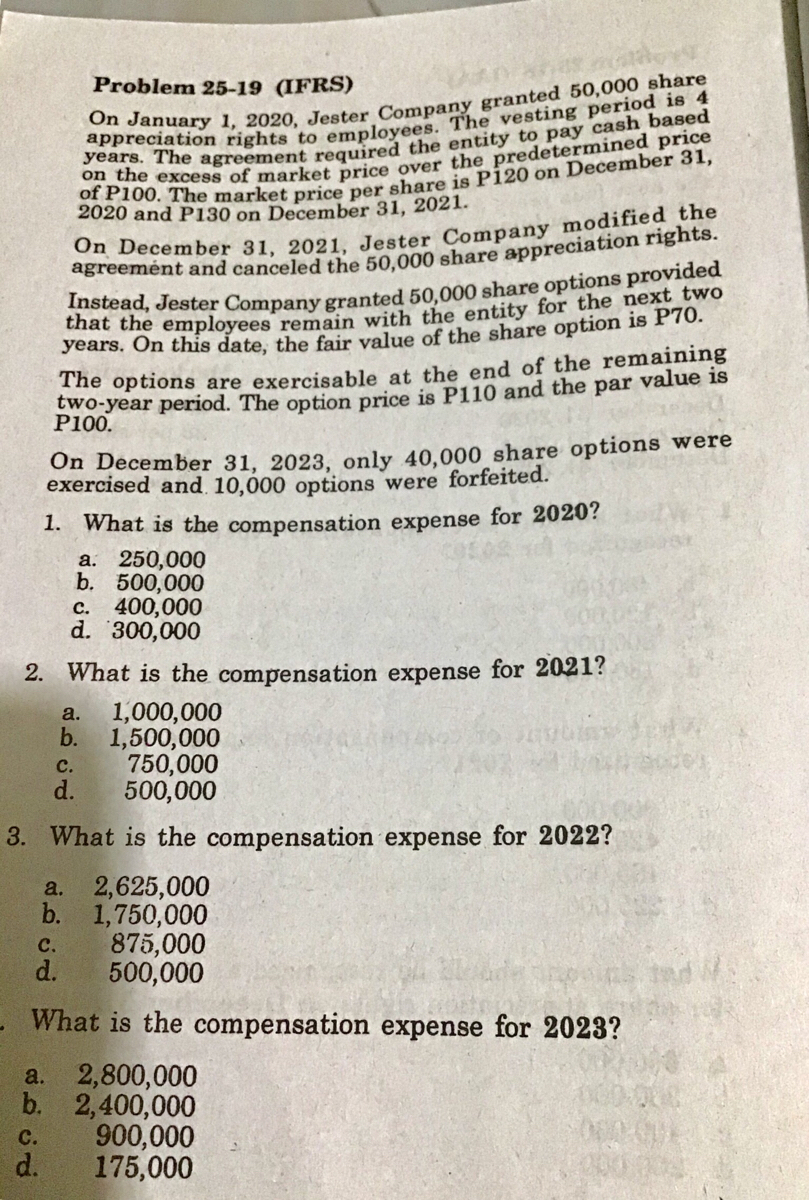

Bond Issuance Costs

Corporations and municipal, state, and federal governments offer debt issues as a means of raising needed funds. Debt issues such as bonds are issued by corporations to raise money for certain projects or to expand into new markets. Municipalities, states, federal, and foreign governments issue debt to finance a variety of projects such as social programs or local infrastructure projects.

The effective interest rate is the rate that exactly discounts the future cash flows of the bond to the net carrying amount at issuance, including the issuance costs. By using this method, companies can ensure that the amortization of issuance costs is proportionate to the interest expense recognized, maintaining consistency in financial reporting. Issuing debt is a corporate action which a company’s board of directors must approve. The interest rate set on the bonds is based on the credit rating of the company and the demand from investors. In contrast, IFRS takes a more integrated approach by deducting bond issuance costs directly from the carrying amount of the bond liability.

When a company or government agency decides to take out a loan, it has two options. This is referred to as a debt issue—the issuance of a debt instrument by an entity in need of capital to fund new or existing projects or to finance existing debt. This method of raising capital may be preferred, as securing a bank loan can restrict how the funds can be used. As a next step in our research on SLHs we plan to assess how they are viewed by various stakeholder groups in the community, including house managers, neighbors, treatment professionals, and local government officials. Interviews will elicit their knowledge about addiction, recovery, and community based recovery houses such as SLHs.

This guarantees that everything we publish is objective, accurate, and trustworthy. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. The interest payments made on bonds, known as coupon payments, are generally tax-deductible for the issuer. For instance, in a low-interest-rate environment, newly issued bonds with higher coupon rates are more attractive, increasing demand and hence their price. Furthermore, loans are usually negotiated directly between the parties involved, while bonds are typically sold on open markets, making them more liquid. This could be a fixed-rate bond, where the interest rate remains constant throughout the term, or a floating-rate bond, where the interest rate varies according to market conditions.

This is especially useful for corporations or governments that need to fund substantial projects, such as expansion initiatives or infrastructure development. Conversely, a bond with a lower credit rating will need to offer a higher interest rate to attract investors willing to take on the additional risk. While both bonds and loans represent debt obligations, there are significant differences between the two. A loan is a direct agreement between a lender and a borrower, often involving collateral, while a bond is a tradable security sold to multiple investors. Before the bonds can be sold, the issuer must obtain approval from the relevant regulatory bodies.